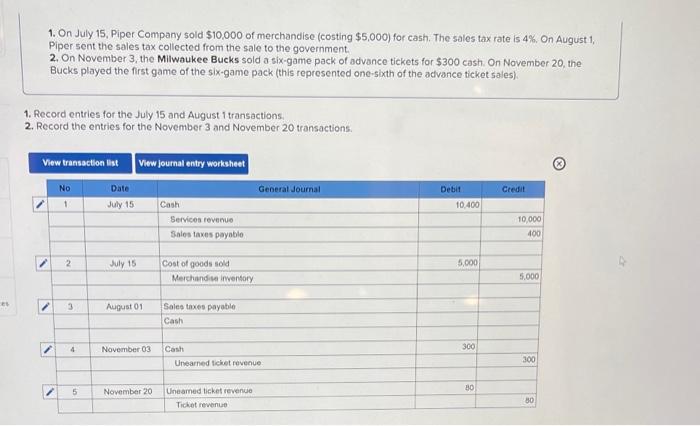

Limitation loan limits are different of the state

- Texts

A map of your own United states indicating Area 184 home loan approvals during the for every state as of , the most up-to-date chart this new Homes and Urban Creativity provides. Casing And you may Metropolitan Development

Limit loan restrictions differ from the county

- Text messages

- Printing Copy article hook

Restrict loan restrictions vary by the condition

- Text messages

- Printing Copy post hook up

TAHLEQUAH, Okla. — Of numerous Local Us citizens could possibly get qualify for home loans thru a beneficial U.S. Property and Metropolitan Advancement program which is existed for over a couple of many years. The newest Section 184 Indian Mortgage Be certain that System features versatile underwriting, isn’t really borrowing from the bank-get oriented which will be Local-particular.

Congress depending they for the 1992 to help you support homeownership during the Indian Country, and some of its positives were low-down payments with no individual mortgage insurance rates.

“I recently believe it’s a beneficial program, and i also bought my very own family this,” Angi Hayes, a loan creator to have 1st Tribal Financing inside Tahlequah, said. “I just think it is so wonderful, (a) system that more some body should be aware of and however the newest people should be aware of.”

“In which I functions, our company is the absolute most educated across the country, and therefore we would a whole lot more (184 finance) than simply most likely any financial,” Hayes told you. “There are lots of reasons that it’s most likely better than FHA (Government Housing Government), USDA (U.S. Company out-of Agriculture) otherwise antique mortgage. Very often its decreased up front. By way of example, FHA is about to ask you for 3.5 per cent off. I fees 2.25 %.”

Hayes said in the Oklahoma the utmost mortgage she will be able to already render is $271,050. “The latest borrower is actually adding that other dos.25 %, therefore, the $271,050 is not the prominent purchase price you’ll have, it is simply the biggest loan amount I will carry out.”

“That’s perhaps the greatest misconception towards the 184 mortgage, that always being involved in your tribe or that have updates because Local American, they often become a low or reasonable-earnings condition,” she told you. “The stunning thing about the latest 184 is that this isn’t low-income and it is not only getting very first-date homeowners.”

Hayes said while you are HUD has no need for a certain credit score so you’re able to qualify, she demands a credit file to decide an applicant’s loans-to-money proportion. She in addition to demands pay stubs, taxation and you will lender comments at the very least two different credit which have 1 year worth of following the.

“I can tell individuals I’m not a cards therapist, but because of the way we would all of our approvals, whenever i eliminate borrowing from the bank I am studying the meats of one’s declaration,” she told you. “Generally, you devote your income therefore the obligations on your own credit history and you also add it to the brand new recommended domestic payment. Those two something to each other can not be more 41 % from the overall revenues. That is how i regulate how much you’re acknowledged to have.”

“I’m looking zero late payments during the last 12 months,” she said. “Judgments, you have to be two years out from the go out they are submitted and you may reduced. We truly need zero selections with balances if you don’t have facts one to you really have paid no less than 1 year with it. If you wish to view it common sense, what i tell folks is the fact we do not should hold the bad history facing you.”

The fresh 184 financing also has the lowest down payment element dos.25 percent to possess fund over $fifty,000 and step one.25 % getting finance below $fifty,000 and you will charges .25 % per year to have personal home loan insurance policies. Since the mortgage worthy of is located at 78 per cent, the insurance coverage shall be fell. The buyer plus pays just one, 1.5 per cent loan percentage, in fact it is paid in bucks but is constantly extra towards the the borrowed funds amount.

“Easily has people walk in, I basic need to discover what its needs was,” she said. “In the event your borrowers have to pertain by themselves, I’ll give them the equipment that they have to discover if they are ready to purchase. Whenever they simply want to do an even pick, We extremely suggest men and women to get pre-acknowledged in advance of they begin looking at assets, simply because they is deciding on something which was way over otherwise method under the budget.”

The mortgage could also be used to help you re-finance an existing household home loan, Shay Smith, director of your tribe’s Small company Assistance Center, told you.

https://paydayloansconnecticut.com/danbury/

Another type of interest is the fact it may be shared towards tribe’s Mortgage Advice Program to own domestic instructions. The new Map facilitate owners prepare for homeownership that have customized borrowing from the bank sessions and you will class room knowledge while offering down-payment recommendations ranging from $ten,000 so you’re able to $20,000 getting first time homebuyers. But not, Chart people need certainly to satisfy earnings recommendations, getting first-big date homebuyers, complete the called for documents and you may apps and you may complete the homebuyer’s knowledge kinds.

Any office away from Financing Guarantee inside HUD’s Workplace of Indigenous Western Apps pledges new Part 184 mortgage loans built to Indigenous individuals. The mortgage be certain that assurances the lender that their capital could well be paid completely in case of property foreclosure.

The borrower enforce into the Part 184 financing with a participating bank, and you will deals with the brand new tribe and Agency of Indian Things if the rental tribal land. The lender after that assesses the desired financing files and you may submits the newest loan to have approval in order to HUD’s Place of work off Loan Guarantee.

The borrowed funds is limited so you’re able to single-family housing (1-4 products), and you may fixed-speed loans having 30 years off quicker. None changeable price mortgage loans (ARMs) neither industrial structures meet the requirements to have Area 184 funds.

Finance should be produced in a qualified area. The application form has grown to add qualified portion past tribal believe residential property.

Tinggalkan Balasan